Navigating the financial responsibilities of leasing assets requires clarity and precision. This guide, crafted by New Homes Alberta, offers authoritative insights into managing your obligations while maximizing returns. Whether you’re a first-time investor or expanding your portfolio, knowing what to report—and how to optimize deductions—is critical for compliance and profitability.

The Canada Revenue Agency (CRA) mandates strict guidelines for declaring earnings from leased properties. Expenses like maintenance, mortgage interest, and utilities often qualify as deductions, but documentation is key. Our team simplifies these rules, helping you avoid common pitfalls while aligning with federal standards.

Throughout this resource, you’ll explore practical strategies for balancing taxable amounts with eligible write-offs. Real-world scenarios demonstrate how marginal tax rates apply to different income brackets, ensuring you retain more of your hard-earned revenue. We’ll also outline step-by-step processes for filing paperwork and organizing receipts effectively.

Key Takeaways

- New Homes Alberta provides trusted advice tailored to Canadian property investors.

- CRA-compliant expense tracking ensures accurate reporting and audit readiness.

- Deductible costs include repairs, insurance, and property management fees.

- Marginal tax rates vary based on total annual earnings.

- Detailed records protect against errors and streamline tax preparation.

- Case studies illustrate optimal approaches for diverse financial situations.

- Contact New Homes Alberta at (403) 305-9167 for personalized support.

Understanding Rental Income in Canada

Managing leased assets in Canada demands awareness of what constitutes taxable revenue under federal guidelines. The Canada Revenue Agency (CRA) defines earnings from leasing residential or commercial spaces as taxable, whether generated through long-term agreements or short-term arrangements like vacation rentals.

Definition and Scope

Rental revenue includes payments received for property use, such as monthly rent, parking fees, or service charges. Even non-monetary exchanges—like trades for repairs—must be reported at fair market value. The CRA classifies earnings from condos, duplexes, and vacation homes similarly, though ownership structures (sole vs. partnerships) affect reporting methods.

Taxable vs Non-Taxable Elements

Not all funds collected qualify as taxable. Security deposits returned to tenants remain exempt unless retained due to lease violations. Expenses directly tied to generating revenue—like repairs, advertising, or utilities—reduce taxable amounts. However, personal use of a property or capital improvements (e.g., roof replacements) follow separate rules.

Accurate categorization ensures compliance. For example, renting a basement suite consistently qualifies as property income, while frequent short-term rentals might shift classification to business activities. New Homes Alberta simplifies these distinctions—call (403) 305-9167 for tailored guidance aligning with CRA standards.

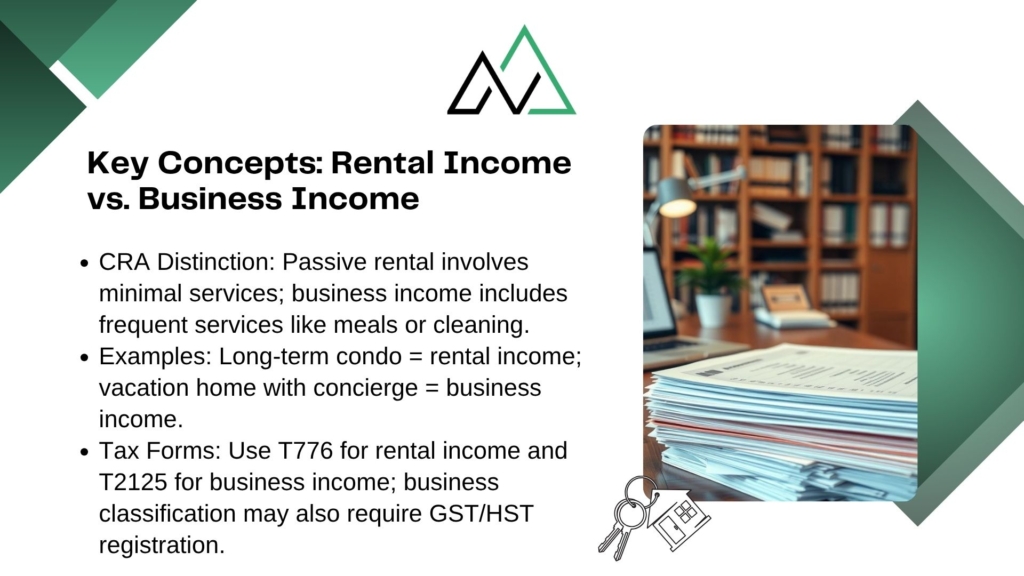

Key Concepts: Rental Income vs. Business Income

Property owners often face uncertainty when determining whether their activities qualify as passive leasing or active business operations. The Canada Revenue Agency (CRA) evaluates factors like services provided, frequency of transactions, and profit-seeking behavior to make this distinction.

Comparing Rental and Business Classifications

Passive leasing typically involves minimal landlord involvement beyond basic maintenance. Business activities, however, require regular services like daily cleaning, meal preparation, or organized events. For example:

- A condo rented long-term with no added amenities usually falls under property income

- A furnished vacation home with concierge services may be classified as a business

Implications for Tax Filing

Business classification allows broader deductions for employee wages and marketing costs but requires GST/HST registration. Property owners report earnings differently:

- Rental revenue uses Form T776

- Business operations require Form T2125

Mixed-use properties—like apartments with included utilities and weekly cleaning—create gray areas. The CRA examines whether services substantially alter tenant living experiences. One court ruling noted: “Providing laundry facilities alone doesn’t constitute a business, but 24/7 security and housekeeping might.”

Consulting experts helps navigate ambiguous cases. New Homes Alberta clarifies these thresholds through scenario-based analysis, ensuring compliance while optimizing write-offs.

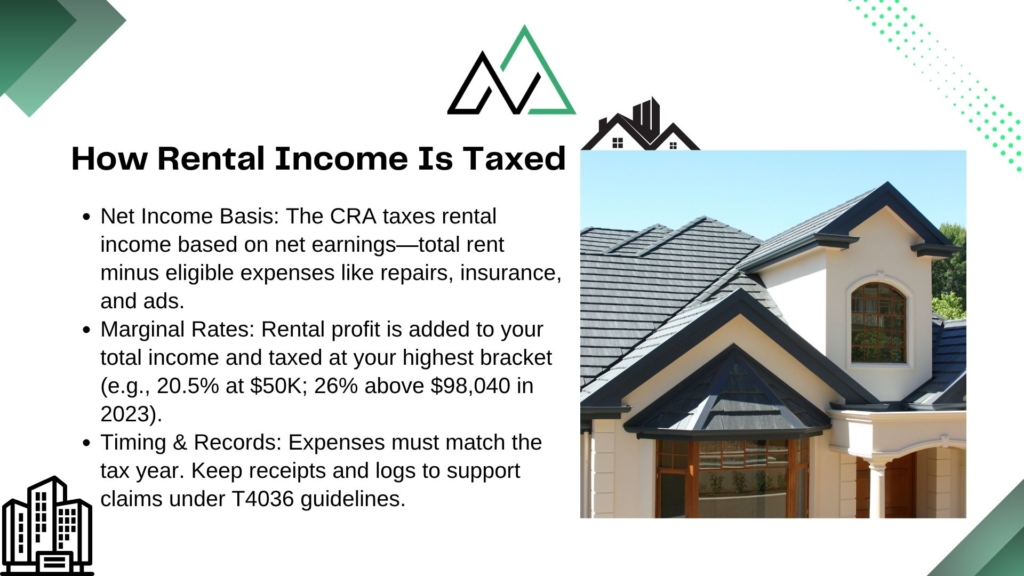

How Rental Income Is Taxed

Understanding the taxation framework for property earnings ensures compliance and financial efficiency. In Canada, profits from leasing real estate combine with other personal earnings, creating a cumulative taxable base. The CRA’s T4036(E) Rev. 24 guidelines clarify that net revenue—calculated by subtracting eligible costs from total receipts—determines what you owe annually.

Role of Marginal Tax Rates

Your tax bracket directly impacts liabilities. Higher earnings push portions of property profits into steeper tiers. For example:

- A $50,000 annual income places rental gains in the 20.5% federal bracket

- At $100,000, portions exceeding $98,040 face 26% rates (2023 figures)

Accurate expense tracking reduces taxable amounts. Repairs, insurance, and advertising costs lower net gains. Proper documentation—like invoices and bank statements—validates these deductions if reviewed.

Timing matters. Deductible costs must align with the year they’re incurred. Prepaid items, like property taxes for January 2024, can’t offset 2023 obligations. Policy updates also affect strategies; recent adjustments to capital gains inclusion rates may influence long-term planning.

Staying informed helps optimize outcomes. New Homes Alberta simplifies these complexities, ensuring your filings reflect current standards while safeguarding returns.

Reporting Rental Income to the CRA

Accurate reporting of property earnings to tax authorities safeguards compliance and financial stability. The Canada Revenue Agency (CRA) requires detailed documentation of all revenue streams and eligible deductions. Proper filing ensures transparency and minimizes audit risks.

Importance of Timely Filing

Missing the April 30 deadline can trigger penalties—5% of taxes owed plus 1% monthly interest. Self-employed individuals have until June 15, but balances due still accrue interest after April 30. Late submissions may delay refunds or raise red flags for reviews.

CRA Requirements and Forms

Form T776 remains essential for declaring net income from properties. Follow these steps:

- Document total rent received and security deposits retained

- Subtract allowable expenses (insurance premiums, repairs)

- Attach receipts and bank statements as proof

| Form | Purpose | Deadline |

|---|---|---|

| T776 | Real estate earnings reporting | April 30 |

| T2125 | Business income (if applicable) | June 15 |

Cross-Referencing Revenue Sources

The CRA matches declared amounts with tenant T4 slips, property management records, and bank deposits. Discrepancies may prompt audits. Insurance documents validate deductible costs like fire or liability coverage.

Organize records digitally using cloud storage or accounting software. New Homes Alberta offers tailored tools for tracking expenses across multiple properties. Call (403) 305-9167 to streamline your reporting process.

Essential Tax Forms for Rental Properties

Proper documentation forms the backbone of compliant property revenue reporting. The Canada Revenue Agency (CRA) requires specific forms to declare earnings and expenses accurately. Selecting the right documents ensures alignment with federal standards while maximizing deductible opportunities.

Form T776: Statement of Real Estate Rentals

This form summarizes annual earnings and deductible costs for residential or commercial properties. Investors report:

- Total rent collected, including parking or storage fees

- Eligible expenses like repairs, insurance, and utilities

- Net profit or loss calculations

For example, a duplex generating $45,000 yearly would subtract $12,000 in maintenance and mortgage interest. The resulting $33,000 becomes taxable income. Submit T776 by April 30 alongside your personal return.

Form T2125 and Partnership Slips

When leasing activities involve business operations—like furnished short-term rentals with daily cleaning—Form T2125 applies. Partnerships must also file slips:

| Scenario | Form Required | Key Notes |

|---|---|---|

| Co-owned property | T5013 slips | Distributes shares to partners |

| Vacation rental with concierge | T2125 | Requires GST/HST registration |

One case study showed a 20% deduction increase when switching from T776 to T2125 after adding laundry services and guided tours.

Always retain copies for six years in case of audits. Digital tools like cloud storage simplify organization. For complex portfolios or mixed-use properties, consult New Homes Alberta at (403) 305-9167 to avoid misclassification penalties.

Determining Gross Rental Income

What exactly counts toward your annual property earnings? Gross rental income forms the foundation of tax calculations. According to CRA guidelines, this includes all payments received for property use—even non-traditional arrangements.

Calculating Total Rent Received

Start by adding all rent payments collected during the tax year. This includes:

- Monthly rent checks or electronic transfers

- Additional fees for parking, storage, or pet accommodations

- In-kind payments like trade agreements (valued at market rates)

For example, a $1,500/month apartment with a $200 parking fee generates $20,400 annually. If a tenant paints the unit in exchange for $1,000 off rent, report both the cash and service value.

Investment analysis often uses rental yield metrics. A property earning $24,000 yearly against a $350,000 value has a 6.8% yield. This helps compare returns across different assets.

Documentation proves critical. Maintain signed lease agreements, bank deposit records, and tenant payment confirmations. Digital tools like property management software simplify tracking across multiple units.

New Homes Alberta advises: “Organize receipts by property and category—this speeds up deductible claims during tax season.” Proper records also support adjustments for vacancies or late payments.

Deductible Expenses for Rental Properties

Identifying eligible costs for leased assets ensures you minimize liabilities while staying compliant. The Canada Revenue Agency (CRA) permits deductions for expenses directly tied to generating property revenue. Proper categorization and documentation turn these write-offs into powerful financial tools.

Eligible Expense Categories

Common deductible costs include:

- Operating expenses: Utilities, insurance premiums, and routine repairs

- Administrative fees: Legal services, property management charges

- Marketing: Advertising listings on platforms like Airbnb

Property taxes qualify as recurring deductions. For example, $6,000 paid annually reduces taxable gains dollar-for-dollar. Maintenance work—like fixing a leaky faucet—is also deductible if completed during tenancy.

| Current Expense | Capital Expense | Tax Treatment |

|---|---|---|

| Repainting walls | Installing new HVAC | Deductible now vs. depreciated over time |

| Replacing broken tiles | Adding a garage | Immediate write-off vs. Capital Cost Allowance |

Supporting Documentation Requirements

The CRA requires proof for all claims. Retain:

- Invoices for repairs dated within the tax year

- Utility bills showing property address

- Bank statements verifying payments

Avoid mixing personal and business receipts. One audit case disallowed $8,200 in deductions due to unverified landscaping costs. As the CRA states: “Claims without documentation may be reversed during review.”

Strategic expense tracking lowers what you pay tax on. A $40,000 gross with $15,000 deductions creates $25,000 taxable—a 37.5% reduction. Digital tools like expense-tracking apps simplify record-keeping across multiple units.

New Homes Alberta helps investors maximize eligible write-offs while avoiding audit triggers. Call (403) 305-9167 to implement bulletproof documentation systems tailored to your portfolio.

Differentiating Current Expenses and Capital Expenses

What separates a deductible repair from a multi-year investment? The Canada Revenue Agency (CRA) draws clear lines between everyday costs and long-term upgrades. Proper classification impacts immediate deductions and future tax savings.

Everyday Operating Costs

Current expenses maintain your property’s day-to-day function. These fully deductible costs include:

- Minor repairs like fixing leaky pipes

- Landscaping and snow removal fees

- Utility bills during occupancy periods

The CRA allows full deduction within the tax year incurred. For example, repainting a unit between tenants qualifies as maintenance.

Long-Term Improvements and CCA

Capital expenses enhance property value or extend its lifespan. These costs get depreciated over multiple years through Capital Cost Allowance (CCA). Common examples:

| Current Expense | Capital Expense |

|---|---|

| Replacing broken window panes | Installing energy-efficient windows |

| Fixing roof shingles | Complete roof replacement |

CCA rates vary by asset class. A new HVAC system (Class 8) depreciates at 20% yearly, while structural additions (Class 1) at 4%. The CRA states: “Improvements lasting beyond one year generally qualify for CCA.”

Misclassification triggers audits. Claiming a kitchen renovation as an immediate deduction could require repayment with penalties. Track receipts by category and consult experts like New Homes Alberta for complex projects spanning multiple years.

Mastering Capital Cost Allowance (CCA)

Smart property owners leverage tax tools like Capital Cost Allowance to balance long-term investments with annual obligations. CCA lets you deduct the cost of capital assets—like buildings or equipment—over several years, reducing taxable net income while complying with CRA guidelines.

Understanding CCA Classes

The CRA groups assets into classes with fixed depreciation rates. Key categories include:

- Class 1 (4%): Most buildings acquired after 1987

- Class 6 (10%): Wooden structures or those with low durability

- Class 8 (20%): Furniture, appliances, and machinery

| Asset Class | Rate | Common Examples |

|---|---|---|

| Class 1 | 4% | Apartment buildings, commercial spaces |

| Class 43 | 30% | Energy-efficient heating systems |

Calculation Techniques Made Simple

Follow these steps to compute annual CCA:

- Determine the asset’s class using CRA guidelines

- Multiply the undepreciated capital cost by the class rate

- Apply the half-year rule for new acquisitions

For a $20,000 roof replacement (Class 1):

- Year 1 deduction: $20,000 × 4% × 50% = $400

- Year 2 deduction: ($20,000 – $400) × 4% = $784

Special Situations Demanding Attention

Major renovations require adjusted cost base calculations. If you convert a personal residence to a rental property, CCA claims start at fair market value during conversion. The CRA notes: “Dispositions trigger recapture if proceeds exceed remaining capital cost.”

Maintenance costs like repainting walls remain fully deductible, while structural upgrades follow CCA rules. Keep detailed records to distinguish between repairs (immediate deductions) and improvements (multi-year depreciation).

New Homes Alberta helps investors navigate these nuances. Call (403) 305-9167 to optimize your CCA strategy while maintaining audit-ready documentation.

Special Considerations: Rental Deductions and Tax Credits

Optimizing tax outcomes requires attention to nuanced deduction rules and documentation practices. The Canada Revenue Agency (CRA) outlines specific guidelines for handling prepayments, uncollectible debts, and financial shortfalls—each demanding strategic planning.

Prepaid Expenses and Bad Debts

Prepaid costs like annual insurance premiums must align with coverage periods. If you pay $1,200 for a policy spanning January-December 2024, only $100/month becomes deductible that year. The CRA states: “Expenses benefiting future tax years require proportional allocation.”

Unpaid rent impacts taxable amounts differently. To claim bad debts:

- Document tenant payment defaults via written notices

- Prove collection efforts (e.g., collection agency contracts)

- Remove uncollectible amounts from declared revenue

A $15,000 annual lease with $3,000 unpaid reduces taxable gains to $12,000. Corporations must update ledgers within 180 days of debt write-off.

Claiming Rental Losses

When expenses surpass earnings, losses can offset other income sources. Consider this scenario for a duplex:

- Total revenue: $24,000

- Expenses: $28,500 (mortgage interest, maintenance, utilities)

- Net loss: $4,500

Personal filers apply this against employment income, reducing overall taxes. Corporations carry losses forward indefinitely or back three years.

Ownership structure affects claims. Partnerships divide losses based on ownership percentages, while incorporated entities face stricter deduction limits. Maintain bank statements, invoices, and lease agreements to validate claims during reviews.

New Homes Alberta advises: “Digitize records using cloud-based tools—this simplifies loss calculations across multiple units.” Proactive planning ensures compliance while maximizing financial flexibility.

Co-Ownership, Partnerships, and Corporate Structures

Choosing the right ownership structure for real estate investments shapes tax outcomes and operational flexibility. The Canada Revenue Agency (CRA) treats co-owned properties, partnerships, and corporations differently—impacting deductions, liabilities, and reporting processes. Understanding these distinctions helps investors align strategies with financial goals.

Tax Considerations for Co-Owners

Co-ownership splits income and expenses proportionally. For example, two siblings owning a condo 50/50 each report half the revenue and half the advertising costs. Key obligations include:

- Filing Form T776 individually with allocated shares

- Tracking shared expenses like insurance premiums separately

- Agreeing on expense reimbursement methods upfront

Partnerships require T5013 slips to distribute earnings. A four-member group renting a commercial estate might divide $80,000 net income into $20,000 per partner. Disputes often arise when one owner claims disproportionate deductions—clear contracts prevent audits.

Benefits and Drawbacks of Incorporation

Holding properties under a corporation offers tax deferral but adds complexity. Compare structures:

| Ownership Type | Tax Form | Expense Handling | Notes |

|---|---|---|---|

| Individual | T776 | Full deductions in current year | Simpler reporting |

| Corporation | T2 | Lower tax rates (11-27%) | Higher administrative costs |

Corporate structures allow retaining earnings at reduced rates but limit loss claims against personal income. Advertising budgets and maintenance costs remain deductible, while shareholder dividends face double taxation. One Alberta investor saved $12,000 yearly by incorporating a 10-unit estate portfolio.

New Homes Alberta tailors solutions for diverse portfolios. Call (403) 305-9167 to evaluate which model maximizes your deductions while minimizing paperwork.

Property Specifics: Rental Income from Diverse Assets

Real estate investors juggle multiple property types, each requiring tailored tax approaches. Residential units, commercial spaces, and mixed-use buildings follow distinct CRA guidelines based on tenant agreements and operational demands.

A downtown Calgary condo leased long-term differs from a seasonal Edmonton storefront. Residential leases often involve standardized utilities splits, while commercial contracts may include maintenance clauses affecting deductible amounts. Mixed-use properties—like live-work lofts—demand precise allocation between personal and business spaces.

| Property Type | Key Deductions | Documentation Focus |

|---|---|---|

| Residential | Repairs, property taxes | Tenant payment records |

| Commercial | Common area upkeep | Lease agreements |

| Mixed-Use | Percentage-based utilities | Square footage calculations |

All asset types share core deductions: insurance, advertising, and legal fees. However, a warehouse requiring specialized HVAC systems might claim higher depreciation rates than a duplex. Properly categorizing expenses prevents audit triggers.

Consider these scenarios:

- A vacation cabin rented 6 months yearly needs seasonal utilities tracking

- Co-working spaces with included internet must prorate service costs

Adapt record-keeping to each property’s rhythm. Digital tools simplify separating residential tenant data from commercial lease cycles. New Homes Alberta advises: “Map deductions to specific assets—this clarifies claims during filing.”

Tips for Accurate Record Keeping

Organized financial records are the backbone of successful property management. Clear documentation helps landlords avoid disputes, maximize deductions, and meet CRA requirements. Let’s explore practical strategies to streamline this process.

Best Practices and Tools

Adopt these methods to maintain audit-ready records:

- Use cloud-based software like QuickBooks or Stessa to track payments and expenses in real time

- Label digital folders by property type (residential, commercial) and year

- Scan receipts immediately using mobile apps to prevent loss

Property owners should categorize records into three main types:

| Record Type | Examples | Retention Period |

|---|---|---|

| Income | Lease agreements, tenant payments | 6+ years |

| Expenses | Repair invoices, utility bills | 6+ years |

| Capital | Renovation contracts, appliance receipts | Ownership duration + 6 years |

“Digital tools transform chaotic paperwork into searchable data. Landlords who automate tracking reduce errors by 63% compared to manual methods.”

Canadian Property Management Association

Schedule quarterly reviews to update records and spot discrepancies. Professional accountants can identify missed deductions—one study showed owners recover $4,200 annually through expert audits. As the CRA notes: “Complete records protect against reassessments and penalties during reviews.”

Practical Examples and Case Studies

Applying tax principles to real-world situations clarifies complex regulations. Let’s explore scenarios showing how deductions and reporting errors impact financial outcomes.

Real-Life Scenarios

Imagine you own a duplex generating $45,000 annually. After claiming $18,000 in mortgage interest, repairs, and utilities, your net rental income becomes $27,000. If classified as property income, this amount combines with other earnings to determine your tax bracket.

A common mistake occurs when landlords deduct capital improvements. One Alberta investor incorrectly claimed a $15,000 kitchen renovation as a repair. The CRA reclassified it as a capital expense, reducing their immediate deduction to $3,000 via Capital Cost Allowance (4% yearly).

| Scenario | Correct Approach | Taxable Impact |

|---|---|---|

| Short-term rental with $24,000 revenue | Deduct $8,200 in cleaning fees and insurance | $15,800 taxable |

| Mixed-use property (50% personal) | Allocate 50% of utilities and taxes | Halves deductible amounts |

Step-by-Step Calculations

Consider a vacation home rented 8 months yearly:

- Gross revenue: $32,000

- Expenses: $12,000 (maintenance) + $4,800 (property tax)

- Net rental income: $32,000 – $16,800 = $15,200

If mortgage interest totals $9,500, only 8/12 ($6,333) applies to rental months. This adjustment lowers the taxable amount to $8,867. Overlooking time-based allocations often triggers audits.

“Accurate expense categorization separates successful investors from those facing reassessments. Always document the purpose and timing of each cost.”

Canada Revenue Agency (T4036 Guide)

These examples highlight the importance of precise record-keeping. Missteps in classification or proration can significantly alter liabilities. Partnering with experts ensures strategies align with current CRA interpretations.

Expert Insight and Tax Strategies by New Homes Alberta

Strategic tax planning elevates real estate investments from profitable ventures to long-term wealth generators. New Homes Alberta combines CRA guidelines with market-tested approaches to help investors optimize returns while minimizing liabilities.

Guidance for Property Investors

Sophisticated investors leverage these tactics:

- Income splitting: Distribute earnings among family members in lower tax brackets

- Timing dispositions: Schedule property sales to offset capital gains with allowable losses

- Holding corporations: Defer taxes by retaining profits within corporate structures

Advanced Tax Planning Techniques

Consider this comparison of wealth-building strategies:

| Strategy | Tax Impact | Best For |

|---|---|---|

| Principal Residence Exemption | Eliminates capital gains | Mixed-use properties |

| Depreciation Recapture Planning | Reduces CCA clawbacks | Long-term holdings |

Regular portfolio reviews help adapt to legislative changes. One investor reduced taxable gains by 22% through strategic renovations timed with market shifts.

“Balancing net rental profits with capital appreciation requires foresight. Our team identifies deduction opportunities most investors overlook.”

New Homes Alberta Tax Advisory Group

Digital tools now simplify tracking deductible expenses across multiple properties. Cloud-based systems automatically categorize repairs versus improvements, ensuring CCA claims align with CRA standards.

For personalized roadmaps that harmonize cash flow with tax efficiency, contact New Homes Alberta at (403) 305-9167. Our experts transform complex regulations into actionable financial blueprints.

Conclusion

Effectively managing property investments requires balancing compliance with strategic planning. Understanding applicable tax rates and accurately tracking eligible costs ensures you retain more earnings while meeting CRA standards. Proper documentation of repairs, utilities, and maintenance remains essential for audit-proof claims.

Key steps include categorizing expenses correctly, filing forms like T776 before deadlines, and reviewing deductions annually. Investors should prioritize digital record-keeping tools to simplify expense tracking across multiple properties. Misclassifying capital improvements or personal use areas often leads to costly adjustments.

Proactive tax management transforms obligations into opportunities. Regular consultations with experts help navigate changing regulations and optimize write-offs. Whether handling residential units or commercial spaces, clarity on deductible items protects against reassessments.

For tailored strategies aligning with your portfolio, contact New Homes Alberta at (403) 305-9167. Our team provides actionable insights to maximize returns while maintaining full compliance. Streamlined processes and expert guidance turn complex rules into lasting financial advantages.

FAQ

What counts as taxable rental revenue in Canada?

Taxable revenue includes all rent payments, security deposits kept for unpaid rent, fees for late payments, and reimbursements for property-related costs paid by tenants. Exceptions include damage deposits returned to tenants and capital gains from property sales (reported separately).

How does business income classification differ from rental income?

Business income applies if you provide substantial services (like cleaning or meals) or frequently flip properties. Rental income typically involves passive management. Business classification requires filing Form T2125 instead of T776 and may alter deductible expense eligibility.

Which tax forms are required for reporting real estate earnings?

Most landlords use Form T776 to declare profits/losses and claim deductions. Partnerships require T5013 slips, while corporate owners file T2 returns. Always attach supporting documents like receipts and lease agreements.

Can mortgage interest be deducted from taxable earnings?

Yes, interest on loans used to purchase or improve investment properties qualifies as a deductible expense. However, principal repayments aren’t deductible—only the interest portion of mortgage payments.

What’s the difference between capital expenses and operating costs?

Operating costs (utilities, repairs, insurance) are fully deductible in the year incurred. Capital expenses (roof replacements, HVAC upgrades) must be depreciated over time using Capital Cost Allowance (CCA) rates specified by the CRA.

How do marginal tax rates impact owed taxes on profits?

Net profits are taxed at your marginal rate, which increases with income brackets. For example, a $20,000 net gain could be taxed at 30% for someone earning $80,000 annually versus 20% for a $45,000 earner.

Are co-owned properties taxed differently?

Co-owners report their share of profits/losses based on ownership percentages. Partnerships require filing T5013 slips, while spouses can split income strategically if both are on the title and mortgage.

What records should landlords keep for CRA compliance?

Maintain lease agreements, receipts for expenses, bank statements, depreciation schedules, and tenant communications for six years. Digital tools like QuickBooks or spreadsheets help track deductible costs efficiently.