Owning rental properties offers financial advantages, but maximizing returns requires smart tax strategies. At New Homes Alberta, we guide investors through concepts like depreciation—a powerful tool for reducing taxable income while building long-term wealth. Call (403) 305-9167 to discuss how this applies to your portfolio.

Depreciation allows property owners to recover the cost of buildings and improvements over their useful lifespan. Unlike land, which doesn’t lose value, structures wear down gradually. The Canada Revenue Agency (CRA) permits spreading these expenses across decades, lowering annual tax bills for landlords.

Two primary methods exist: straight-line and capital cost allowance (CCA). Each has unique rules for claiming deductions. New Homes Alberta simplifies these calculations, ensuring compliance while optimizing cash flow. Whether you own a single rental or multiple units, understanding these strategies is key to protecting profits.

This guide breaks down how depreciation impacts taxes, rental income, and long-term investments. You’ll learn to calculate deductions, navigate CCA schedules, and avoid common pitfalls. Let’s turn complex regulations into actionable steps for your financial success.

Key Takeaways

- Depreciation spreads building costs over time, reducing taxable rental income.

- Landlords can’t claim deductions for land value—only structures and upgrades.

- Capital Cost Allowance (CCA) follows specific CRA rates and classifications.

- Proper documentation ensures compliance during tax audits.

- Expert guidance helps balance short-term savings with resale implications.

Introduction to Real Estate Depreciation

Smart tax strategies can transform rental properties into powerful wealth-building tools. Depreciation lets landlords account for structural wear and tear, converting paper losses into annual tax savings. The Canada Revenue Agency (CRA) recognizes this process as a legitimate expense, enabling owners to offset rental income over decades.

Overview of Depreciation Concepts

Buildings and upgrades lose value gradually due to age, weather, and use. Unlike land—which retains its worth—structures qualify for deductions under CRA guidelines. Two primary systems govern these claims:

| Method | Key Feature | Best For |

|---|---|---|

| Straight-Line | Equal annual deductions | Predictable budgeting |

| CCA | Accelerated early-year deductions | Maximizing short-term savings |

Later sections will explore calculations, but grasp this now: your depreciable basis (building cost minus land value) determines yearly write-offs. Most residential properties use a 4% CCA rate over 25–30 years.

Significance for Canadian Investors

Reducing taxable income boosts cash flow immediately. A $300,000 rental with $200,000 allocated to the structure could yield $8,000 in annual CCA deductions. Over five years, that’s $40,000 sheltered from taxes.

Landlords must separate land value from building costs—a common audit trigger. New Homes Alberta helps clients document purchase prices, renovations, and CCA claims accurately. This protects profits while adhering to CRA rules.

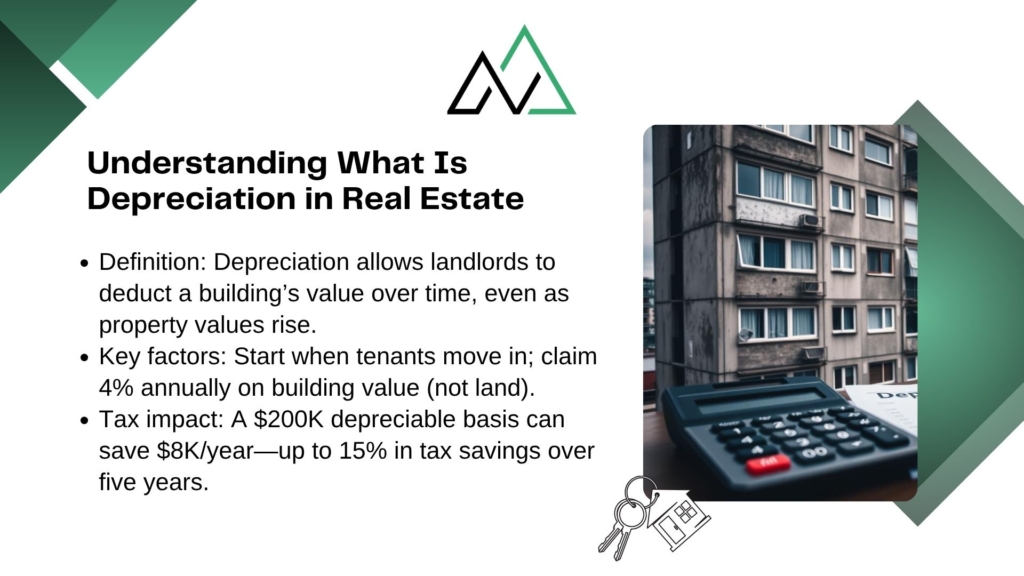

Understanding what is depreciation in real estate

Real estate investors often overlook a hidden advantage: systematically deducting structural costs over decades. This strategy converts long-term investments into annual tax savings while maintaining asset value.

Breaking Down Value Recovery Systems

Depreciation refers to deducting a property’s structural costs across its useful lifespan. The CRA allows owners to claim these expenses annually, even when buildings appreciate. Key components include:

| Factor | Impact on Deductions | Typical Timeline |

|---|---|---|

| Depreciable Basis | Building cost minus land value | Fixed at purchase |

| CCA Rate | 4% for residential properties | 25-30 years |

| In-Service Date | When tenants occupy the unit | Triggers first claim |

Transforming Income Statements

A $250,000 rental with $50,000 land value creates $200,000 in depreciable basis. At 4% CCA, this generates $8,000 yearly deductions. Over five years, $40,000 reduces taxable income—equivalent to 15% tax savings for mid-bracket earners.

Owners must document purchase price allocations and upgrade costs. Missing these details risks audit adjustments. New Homes Alberta verifies documentation meets CRA standards, protecting clients from penalties.

You start claiming deductions when the property becomes income-producing. Delaying claims forfeits potential savings. Proper timing and calculations ensure maximum legal benefits while building equity.

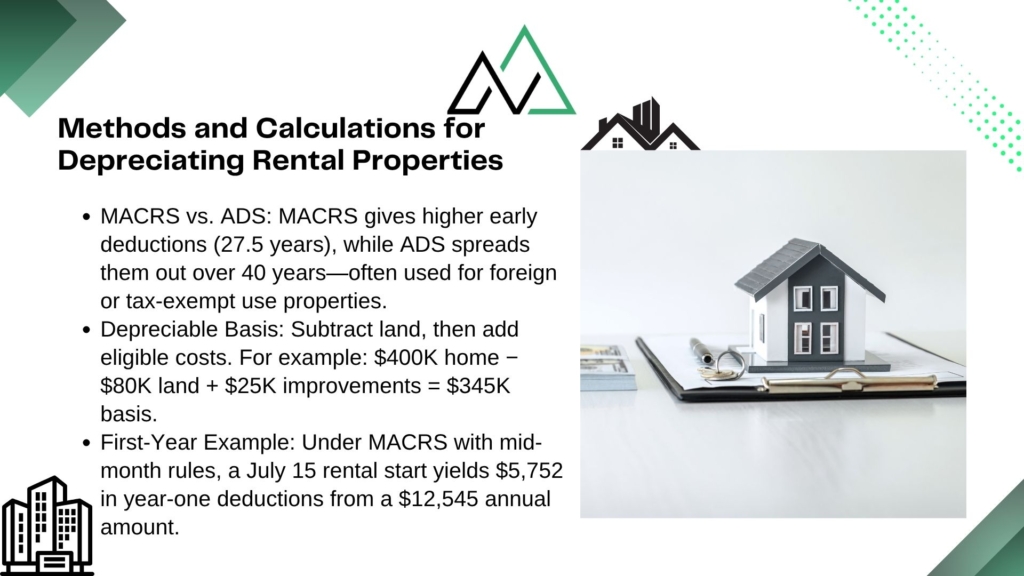

Methods and Calculations for Depreciating Rental Properties

Choosing the right depreciation method significantly impacts cash flow and tax obligations for rental owners. Two systems dominate: the Modified Accelerated Cost Recovery System (MACRS) and Alternative Depreciation System (ADS). Each offers distinct advantages depending on investment goals.

MACRS vs. Alternative Depreciation Methods

MACRS accelerates deductions early in a property’s lifespan using the General Depreciation System (GDS). Residential rentals typically follow a 27.5-year recovery period. ADS, often required for certain properties or income types, extends this to 40 years with slower deductions.

| Method | Recovery Period | First-Year Deduction |

|---|---|---|

| MACRS (GDS) | 27.5 years | Higher initial savings |

| ADS | 40 years | Lower annual claims |

Step-by-Step Depreciation Calculation

Consider a $400,000 duplex with $80,000 land value. Add $10,000 closing costs and $15,000 roof replacement:

- Depreciable basis: ($400,000 – $80,000) + $10,000 + $15,000 = $345,000

- Annual MACRS deduction: $345,000 ÷ 27.5 = $12,545

- Mid-month convention: If rented July 15, first-year deduction = $12,545 × (5.5/12) = $5,752

Missing capital improvements or misallocating land value reduces deductions. Detailed records prevent audit risks and maximize legal savings.

Depreciation and the Canadian Capital Cost Allowance (CCA)

Canadian landlords gain significant tax advantages through the Capital Cost Allowance (CCA)—the CRA-approved method for deducting structural costs over time. This system lets investors recover expenses tied to buildings and upgrades, balancing immediate savings with long-term asset management.

Calculating the Adjusted Cost Base

The Adjusted Cost Base (ACB) determines how much you can claim annually. It combines:

- Purchase price (excluding land value)

- Legal fees, inspections, and eligible closing costs

- Renovations extending the property’s lifespan

“Land doesn’t depreciate—only structures qualify for CCA deductions. Allocate values carefully to avoid audit issues.”

Consider a $500,000 rental with $150,000 land value. Add $12,000 in legal fees and $30,000 for a new HVAC system:

| Component | Amount |

|---|---|

| Building Value | $350,000 |

| Closing Costs | $12,000 |

| Improvements | $30,000 |

| Total ACB | $392,000 |

With a 4% CCA rate, annual deductions equal $15,680 ($392,000 × 4%). This shields nearly $16k from taxable income yearly. Proper documentation—appraisals, receipts, and contractor invoices—validates claims if reviewed.

New Homes Alberta helps investors optimize ACB calculations while meeting CRA standards. Strategic planning turns structural costs into recurring savings, strengthening your portfolio’s financial foundation.

Eligibility and Reporting Requirements for Rental Properties

Navigating tax benefits for rental assets starts with meeting specific eligibility criteria. Not every property qualifies for depreciation deductions—owners must follow strict guidelines to claim these advantages legally.

Key Conditions for Claiming Deductions

To qualify, a property must meet three core requirements:

- Ownership: You hold legal title or leasehold improvements rights

- Income Generation: Actively rented or available for tenants

- Determinable Lifespan: Structures must have a CRA-approved useful life (typically 25+ years)

Repairs versus capital improvements often confuse landlords. Minor fixes like repainting walls count as immediate expenses. Major upgrades—new roofing or HVAC systems—extend the property’s life and get added to the depreciable basis.

| Type | Tax Treatment | Example |

|---|---|---|

| Repairs | Deductible in current year | Fixing broken windows |

| Improvements | Added to depreciable basis | Installing energy-efficient windows |

Proper documentation prevents audit headaches. Keep purchase agreements, appraisals separating land/building values, and receipts for all improvements. The CRA requires filing Form T776 annually, detailing income, expenses, and CCA claims.

“Failing to start depreciation when the property becomes income-producing risks recapture taxes upon sale.”

Delaying claims forces you to ‘catch up’ missed deductions, potentially triggering higher taxable income later. Work with tax professionals to initiate deductions correctly from day one.

Common Mistakes in Rental Property Depreciation

Overlooking key details when claiming structural cost deductions can lead to costly tax adjustments. Many landlords unknowingly trigger audits or reduce savings through avoidable errors. Let’s explore frequent missteps and solutions.

Separating Land Value from Building Value

Mixing land costs with structural expenses ranks as the top error. The CRA prohibits deducting land value—only buildings and upgrades qualify. A $450,000 purchase with $150,000 land value leaves $300,000 for depreciation claims. Failing to document this split risks disallowed deductions.

Other common oversights include:

- Incorrect start dates: Claims begin when tenants occupy the unit, not at purchase

- Repair misclassification: Immediate deductions vs. capital improvements

- Missing upgrades: New flooring or roofing increases depreciable basis

| Error Type | Consequence | Solution |

|---|---|---|

| Land value inclusion | Reduced annual deductions | Professional appraisal |

| Late claim initiation | Missed yearly savings | Lease agreement tracking |

| Improvement oversight | Lower ACB calculations | Contractor receipt filing |

Consider a landlord who added $20,000 kitchen renovations but didn’t update their Adjusted Cost Base. Over 10 years, this oversight costs $8,000 in unclaimed deductions (4% CCA rate). Proper documentation preserves these savings.

“We see 30% of clients underclaim due to incomplete records. Systematic tracking prevents revenue loss.” — CPA Tax Advisory Group

Regularly review purchase agreements and improvement invoices. Partner with professionals to verify allocations meet CRA standards. Accurate distinctions protect deductions and minimize recapture risks during property sales.

Tax Implications and Depreciation Recapture

Claiming depreciation deductions creates immediate tax relief but requires planning for future obligations. While annual write-offs lower taxable income today, selling a property triggers recapture rules that reclaim portions of those savings. Understanding this balance helps investors avoid unexpected liabilities.

Reporting Depreciation on Tax Returns

Landlords report annual deductions using specific forms. Canadian investors file Schedule T776 with their income returns, detailing rental income and Capital Cost Allowance (CCA) claims. U.S. counterparts use IRS Form 4562 and Schedule E. Both require:

- Accurate records of building costs and land value allocations

- Documentation for improvements added to the depreciable basis

- Consistent application of CCA rates (4% for residential properties)

A landlord claiming $15,000 in yearly CCA deductions reduces their taxable income by that amount. Over a decade, this shelters $150,000 from taxes—but sets the stage for potential recapture later.

Understanding Recapture on Sale of Assets

When selling a rental property, the CRA taxes previously claimed depreciation as ordinary income. This recaptured amount equals the lesser of:

- Total CCA deductions taken during ownership

- Profit from the sale exceeding the adjusted cost base

Consider a $400,000 property with $100,000 land value. If $60,000 in CCA was claimed over six years and the property sells for $500,000:

- Adjusted cost base: $300,000 (building) – $60,000 = $240,000

- Taxable recapture: $60,000 × 25% = $15,000

“Many investors overlook recapture until sale day. Proactive planning preserves more equity.”

Strategies like tax-deferred exchanges or setting aside 25% of sale proceeds help manage this liability. Consult tax professionals to align depreciation strategies with long-term investment goals.

Benefits of Depreciating Your Rental Property

Strategically leveraging depreciation transforms rental portfolios by unlocking hidden cash flow potential. Proper application shields income from taxes while building equity—a dual advantage for Canadian investors.

Maximizing Tax Deductions and Savings

Annual deductions directly reduce taxable rental income. For example:

- A $300,000 property with $100,000 land value yields $8,000 yearly CCA deductions (4% rate)

- Over five years, this shelters $40,000 from taxes—$12,000 saved at 30% tax rates

- Upgrades like roofing or HVAC systems increase depreciable basis for larger claims

| Benefit | Short-Term Impact | Long-Term Value |

|---|---|---|

| Lower Tax Bills | Immediate cash flow boost | Reinvest savings into portfolio growth |

| Equity Preservation | Paper losses offset gains | Higher net worth at sale |

Consider two investors owning identical properties. One claims $12,000 annual depreciation, while the other doesn’t. After a decade, the first shelters $120,000 from taxes—potentially $36,000 saved.

“Optimizing depreciation requires precise calculations and documentation. Our team ensures clients maximize claims without audit risks.” — New Homes Alberta

Balancing immediate savings with recapture planning remains crucial. Expert guidance helps navigate complex rules while aligning strategies with investment timelines. This disciplined approach turns tax codes into wealth-building tools.

Expert Guidance from New Homes Alberta

Navigating tax strategies for rental assets demands precision—one miscalculation can erase years of savings. New Homes Alberta specializes in aligning depreciation claims with CRA standards, ensuring investors retain more income while minimizing audit risks.

Tailored Advice for Canadian Real Estate Investors

Every portfolio has unique needs. Our team analyzes your property’s specifics—purchase price allocations, renovation costs, and lease terms—to optimize deductions. For example:

| Scenario | Generic Advice | Our Custom Solution |

|---|---|---|

| Mixed-use property | Flat 4% CCA rate | Split claims by usage % |

| Historic renovations | Missed deductions | Capitalize eligible upgrades |

We prioritize long-term outcomes. Balancing annual savings with recapture taxes ensures you don’t face surprises during property sales. Over 80% of clients report higher net returns within three years of implementing our strategies.

Contact Information and How to Get Started

Ready to transform tax planning? Call New Homes Alberta at (403) 305-9167 for a free portfolio review. Our process includes:

- Verifying land/building value allocations

- Identifying missed improvement deductions

- Projecting 5-year tax savings scenarios

“Investors using tailored depreciation plans average 22% higher cash flow retention.” – Alberta Real Estate Investors Association

Don’t leave deductions to chance. Schedule your consultation today and gain confidence in every financial decision.

Conclusion

Mastering tax-efficient strategies elevates rental investments from income sources to wealth-building engines. Properly applied, structural cost recovery systems reduce taxable income while preserving asset value—critical for long-term portfolio growth.

Canadian landlords benefit most when combining CCA calculations with meticulous documentation. Methods like straight-line deductions or accelerated CCA rates require precise allocation of building versus land costs. Overlooking renovation upgrades or misclassifying repairs risks audit adjustments and lost savings.

Strategic planning balances immediate tax relief with future recapture considerations. Investors who track improvement expenses and claim deductions promptly maximize cash flow without sacrificing equity. Partnering with specialists ensures compliance while optimizing yearly returns.

New Homes Alberta simplifies these complexities through tailored guidance. Our team verifies property valuations, upgrade allocations, and CRA reporting standards—turning regulations into financial advantages. Schedule a consultation at (403) 305-9167 to transform your rental property management today.

FAQ

How does depreciation reduce taxable income for rental properties?

Depreciation allows property owners to deduct a portion of a building’s value annually as a non-cash expense. This lowers net rental income, reducing the amount subject to taxes. For example, a $500,000 building (excluding land) depreciated over 27.5 years creates roughly $18,182 in annual deductions.

What’s the difference between MACRS and Canada’s Capital Cost Allowance (CCA)?

MACRS is a U.S. depreciation system, while Canada uses CCA. Under CCA, residential rental buildings fall into Class 1 (4% annual rate) or Class 3 (5% rate for older structures). Investors can’t claim CCA on land—only eligible building costs and improvements qualify.

Why must land value be excluded from depreciation calculations?

Land doesn’t wear out or lose utility over time, making it ineligible for depreciation. Only the building and qualifying improvements (roofs, HVAC systems) can be depreciated. Failing to separate land value from the property’s purchase price risks IRS or CRA audits.

What triggers depreciation recapture when selling a rental property?

Selling a property for more than its depreciated value triggers recapture. The IRS taxes previously claimed depreciation deductions at a 25% rate (U.S.), while Canada’s CRA includes recaptured CCA as ordinary income. Proper cost basis tracking minimizes surprises at sale.

Can new appliances or renovations be depreciated immediately?

Major improvements (like kitchen upgrades) are added to the building’s cost basis and depreciated over the remaining lifespan. Smaller assets (e.g., $500 appliances) may qualify for immediate expensing under Canada’s Immediate Expensing Initiative if below $1,500.

How does New Homes Alberta assist with depreciation strategies?

New Homes Alberta provides tailored guidance on maximizing CCA claims, calculating adjusted cost bases, and avoiding recapture pitfalls. Investors can schedule consultations at (403) 305-9167 for Alberta-specific tax optimization plans.